Global funding dynamics are shifting dramatically as artificial-intelligence (AI) startups gobble up a growing share of venture-capital (VC) investments. According to recent data, AI-related companies accounted for over half of all VC funding in early 2025, marking a major turning point in the tech investment landscape.

The Numbers Tell the Story

-

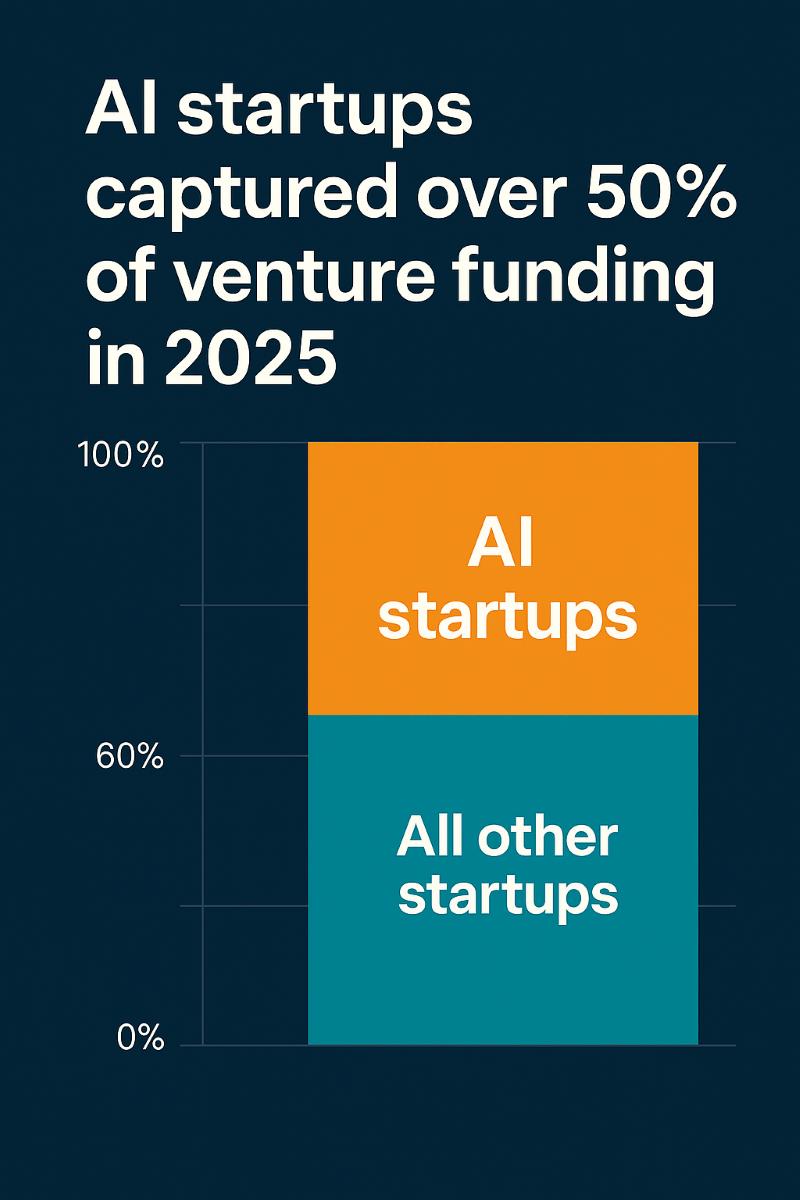

In the first half of 2025, AI-related targets took approximately 51 % of total VC deal value, up from single-digit shares just a few years ago.

-

In the U.S., the share was even higher: AI startups captured about 64 % of VC funding in the corresponding period.

-

Multiple sources highlight that large funding rounds (often $500 million or more) are disproportionately going to AI and AI-infrastructure companies rather than broad, early-stage tech startups.

What’s Driving the Surge?

-

Mega-rounds and concentration: A small set of startups are raising enormous rounds, which drives the aggregate share of AI funding higher, even as the number of deals may flatten. For example, several firms raised funding in the billions of U.S. dollars.

-

Infrastructure & model demand: As AI moves from concept to deployment, back-end infrastructure (compute, data, model training) attracts heavy investment. Many VCs see AI as the next frontier of industrial transformation.

-

Selective investor behaviour: With macro uncertainty and a tougher fundraising environment for new VC funds, limited partners (LPs) are favouring proven startups in AI, deep tech, and model-driven companies. This leads to a bifurcation: winners get big, many others struggle.

Implications for Startups & Investors

-

For early-stage startups, the environment is more challenging: unless the business has strong traction, differentiated IP or model capability, funding may be harder to come by. Investors are demanding clarity on path to scale and profitability.

-

For investors, the concentration means risk is also concentrated: when large rounds dominate the landscape, valuations can become inflated, and the gap between winners and the rest deepens.

-

For the ecosystem, the dominance of AI investment raises questions about balance: Will other sectors (fintech, clean-tech, biotech) get sidelined? Will innovation become narrower? Some reports warn of this risk.

Regional & Sector Highlights

-

The U.S. remains the epicentre of AI investment, drawing the majority of large rounds.

-

Within the U.S., certain cities like the Bay Area dominate: one report shows the Bay Area captured 51% of AI funding among U.S. metros in a recent period.

-

Sector-wise, vertical AI applications (eg: industry-specific models, health-AI, enterprise AI) are gaining ground, not just generic horizontal models.

Looking Ahead

While the momentum is strong, a few caveats remain:

-

Valuation risk: Some mega-rounds may have inflated valuations which could lead to corrections.

-

Regulatory & ethical pressure: As AI becomes more embedded in the economy, issues of governance, data-privacy and algorithmic risk will become more acute. Startups must be ready.

-

Innovation diffusion: The sector needs to ensure that investment isn’t just pouring into a few outliers. Broader innovation in AI, across regions and sectors, will determine long-term health.

-

Exit environment: While funding is high, startups must still deliver results. IPOs, acquisitions and exits will be key to sustaining this investment wave.