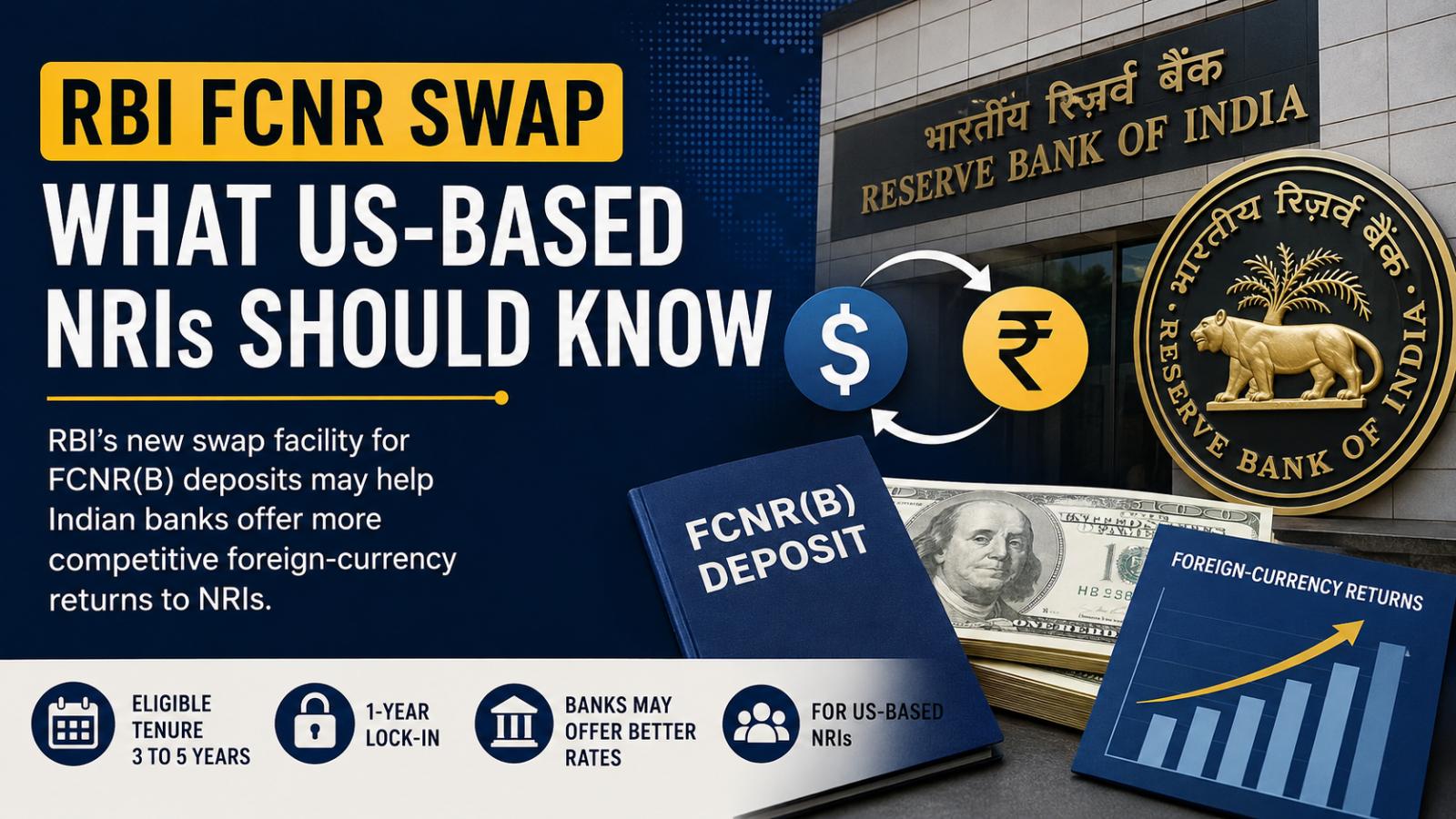

The RBI introduced the US dollar-rupee swap facility on Monday, June 8, 2026. It applies to eligible fresh FCNR(B) deposits, including deposits renewed at maturity, with an original tenure of at least three years and no more than five years.

Deposits must be mobilized between Monday, June 8, 2026, and Wednesday, September 30, 2026. Banks may use the RBI swap window through Friday, October 16, 2026.

The swap period must align with the underlying deposit. Banks may price eligible deposits under their internal policies while remaining within applicable RBI limits.

What the RBI Facility Covers

In a clarification issued Tuesday, June 23, 2026, the RBI said the swap covers only the deposit principal and not the interest.

Deposits included in the scheme carry a one-year lock-in. After that period, a bank may permit early withdrawal under its own policy, but the associated RBI swap cannot be canceled.

FCNR(B) accounts allow eligible nonresident customers to hold term deposits in permitted foreign currencies rather than converting the money into Indian rupees. This can reduce direct exposure to rupee depreciation on the deposited amount.

What US-Based NRIs Should Compare

Rates may differ by bank, currency, deposit size and maturity. Before transferring funds, customers should compare compounding, minimum-deposit requirements, early-withdrawal penalties, loan options and the treatment of interest.

The RBI policy does not guarantee higher returns or a specific level of foreign-currency inflows. Actual benefits will depend on bank pricing, global interest rates, market conditions and depositor demand.

US-based NRIs should confirm current terms directly with a regulated bank and review any applicable US tax or reporting obligations before investing.