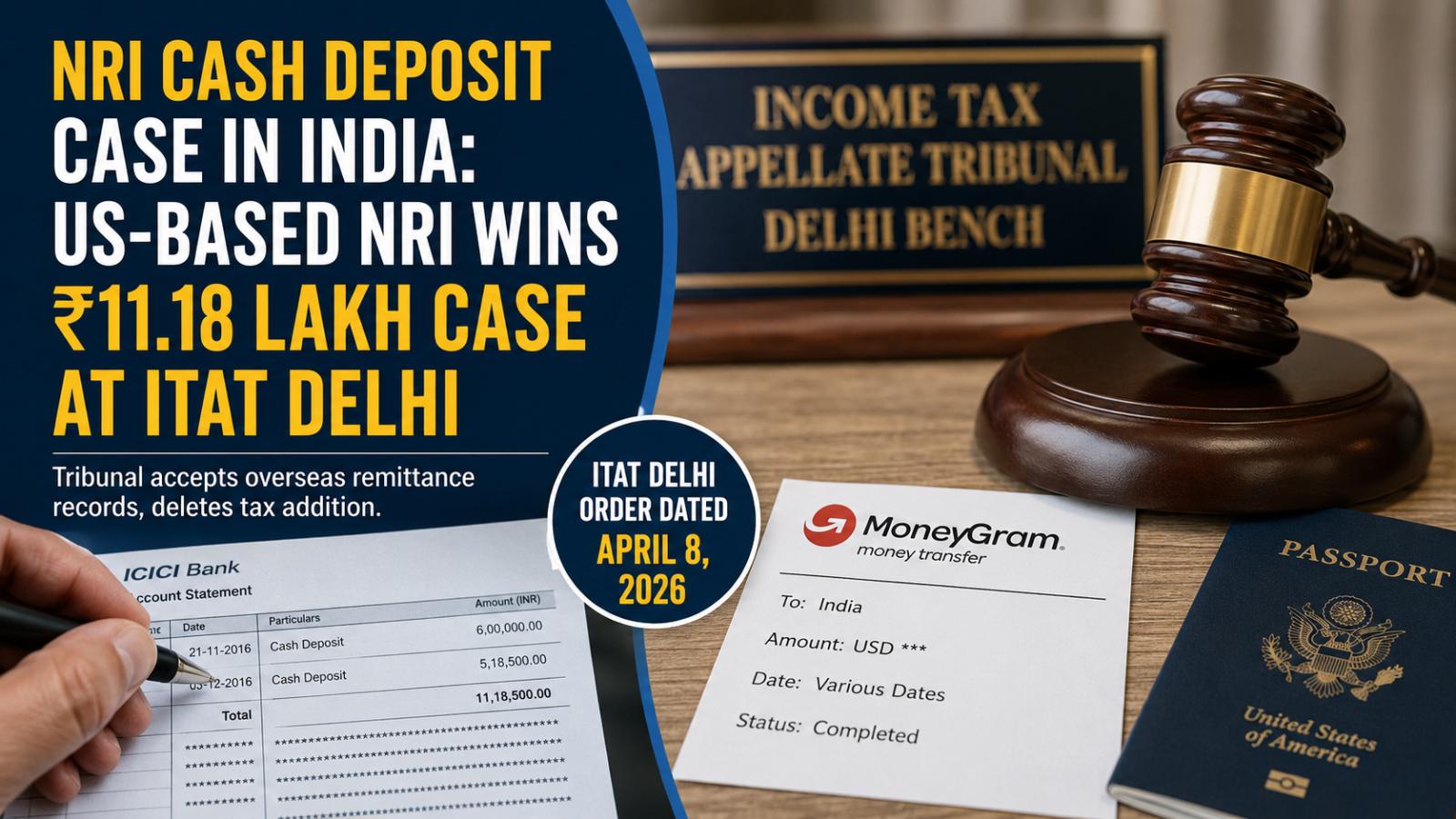

A US-based NRI won relief in an NRI cash deposit tax case in India after the Delhi bench of the Income Tax Appellate Tribunal accepted that ₹11.18 lakh deposited during demonetisation came from earlier overseas remittances intended to support his parents.

In an order pronounced on Wednesday, April 8, 2026, in Arun Bussi v. ACIT, the tribunal directed the deletion of the tax addition for assessment year 2017-18. The dispute concerned ₹11,18,500 deposited into an ICICI Bank account on November 21 and December 3, 2016.

ITAT Delhi Accepts NRI Cash Deposit Explanation

Bussi, a US citizen working in the United States, said he had sent money to his parents through MoneyGram and had also brought funds during visits to India. His parents retained some of the money in cash for their needs.

During a visit following India’s November 8, 2016, demonetisation announcement, he found that the accumulated money remained with his parents and deposited it into his Indian bank account.

The assessing officer rejected his explanation. The tribunal, however, considered his affidavit, MoneyGram receipts, US bank records and passport-linked travel details. It also noted that tax authorities had not identified another source of income that could explain the deposit.

The ITAT concluded that the amount should be treated as coming from disclosed sources and directed that the addition be deleted. Both connected appeals, ITA Nos. 231/Del/2021 and 2171/Del/2023, were allowed.

What the NRI Cash Deposit Ruling Means

The decision does not provide blanket protection for NRI cash deposits. It also should not be presented simply as a ruling that every gift to parents is tax-free.

Its practical lesson is narrower: overseas Indians should preserve remittance receipts, bank statements, income records, passport details and documents explaining why money was held or deposited.

For NRIs supporting parents in India, traceable records and formal remittance channels can become crucial when tax authorities question a high-value transaction. The ruling matters because it shows that the complete source and circumstances of a deposit—not the cash amount alone—can influence the outcome of a tax dispute.