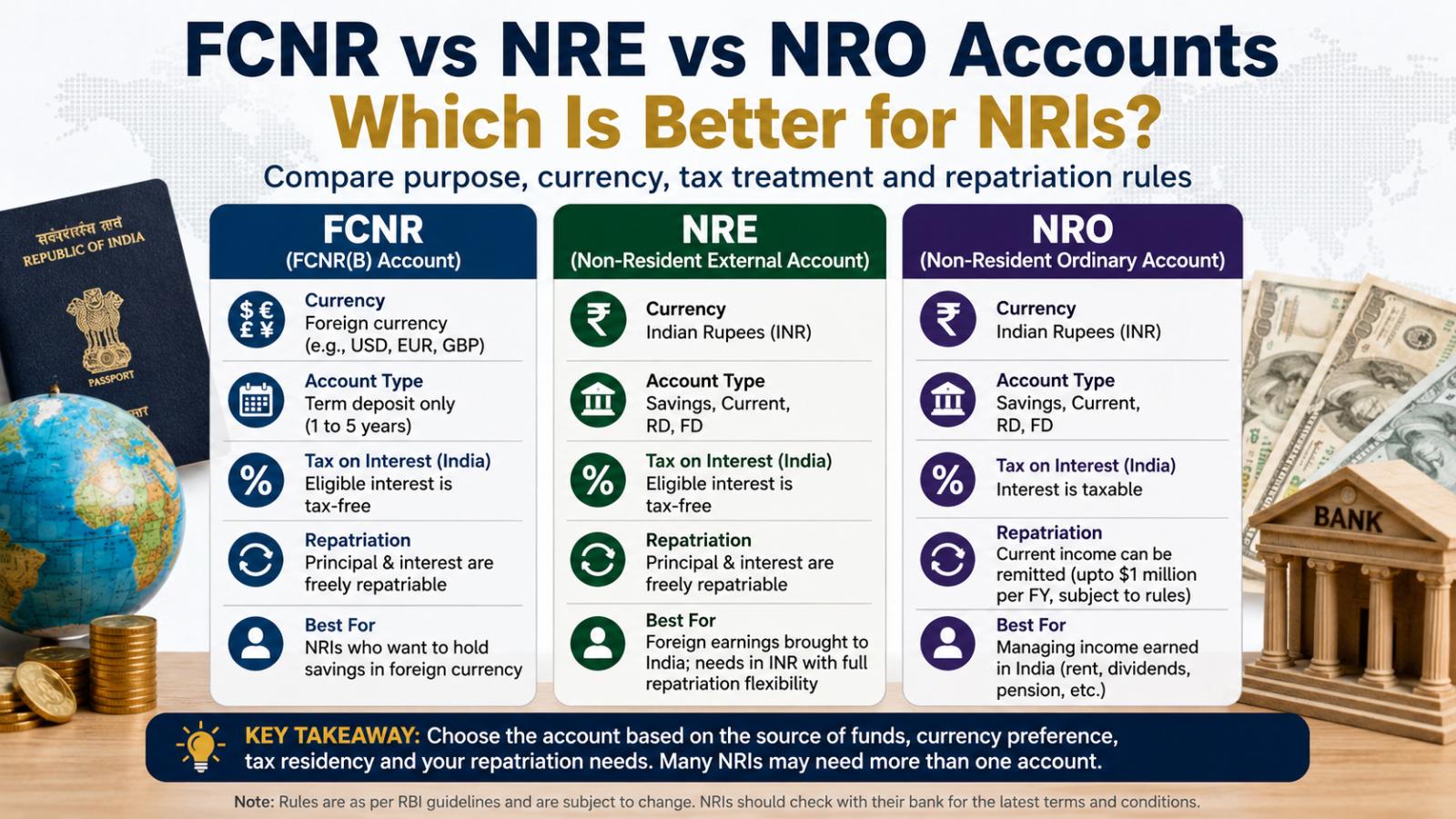

FCNR vs NRE vs NRO accounts serve different purposes. The right choice generally depends on where the money was earned, which currency the depositor wants to hold and how easily the funds must move outside India.

There is no single account that is best for every NRI.

The RBI is encouraging banks to attract more foreign-currency deposits, although most NRI bank money in India remains in rupee-denominated accounts. Read our analysis of why the RBI is pushing for more FCNR deposits.

FCNR vs NRE vs NRO Accounts: Key Differences

FCNR: For Holding Savings in Foreign Currency

A Foreign Currency Non-Resident, or FCNR(B), account is a term deposit maintained in a permitted foreign currency rather than Indian rupees.

It may suit NRIs who want to place overseas savings with an Indian bank without converting the principal into rupees. FCNR deposits generally run from one to five years, and both principal and interest are repatriable.

Eligible interest is exempt from Indian income tax while the account holder meets the applicable residency conditions. Early withdrawal rules matter: no interest is payable when an FCNR deposit is withdrawn before completing the minimum one-year period.

U.S.-based NRIs considering an FCNR deposit can also compare FCNR deposits and U.S. CDs by interest rates, taxation, liquidity and deposit-insurance protection.

NRE: For Foreign Earnings Converted Into Rupees

A Non-Resident External account holds money in Indian rupees. It can receive eligible overseas remittances and may be opened as a savings, current, recurring or fixed-deposit account.

NRE accounts may work better for NRIs who need rupees for expenses or investments in India while retaining the ability to repatriate the balance. Eligible interest remains exempt from Indian income tax, but the account holder is exposed to rupee movements when converting money back into dollars or another foreign currency.

NRO: For Income Earned in India

A Non-Resident Ordinary account is mainly used to manage income received in India, including rent, dividends, pensions and other legitimate dues.

NRO accounts are rupee-denominated, and their interest is taxable in India. Current income may be sent abroad after applicable requirements are met. NRIs and eligible overseas Indians may also remit qualifying balances up to $1 million per Indian financial year, subject to taxes, documents and RBI conditions.

Which Account Should an NRI Choose?

FCNR may fit foreign-currency savings that can remain deposited for at least one year. NRE may suit overseas earnings needed in rupees with broad repatriation flexibility. NRO is generally the appropriate account for receiving and managing Indian-source income.

Many NRIs may need more than one account because overseas earnings and Indian income are treated differently.

For U.S. citizens and resident aliens, Indian tax exemption does not automatically make the interest tax-free in the United States. Foreign interest generally forms part of worldwide income, and accounts may trigger FBAR or other reporting requirements.

The best account therefore depends less on the advertised interest rate and more on the source of the money, currency risk, access needs, tax residency and plans for repatriation.