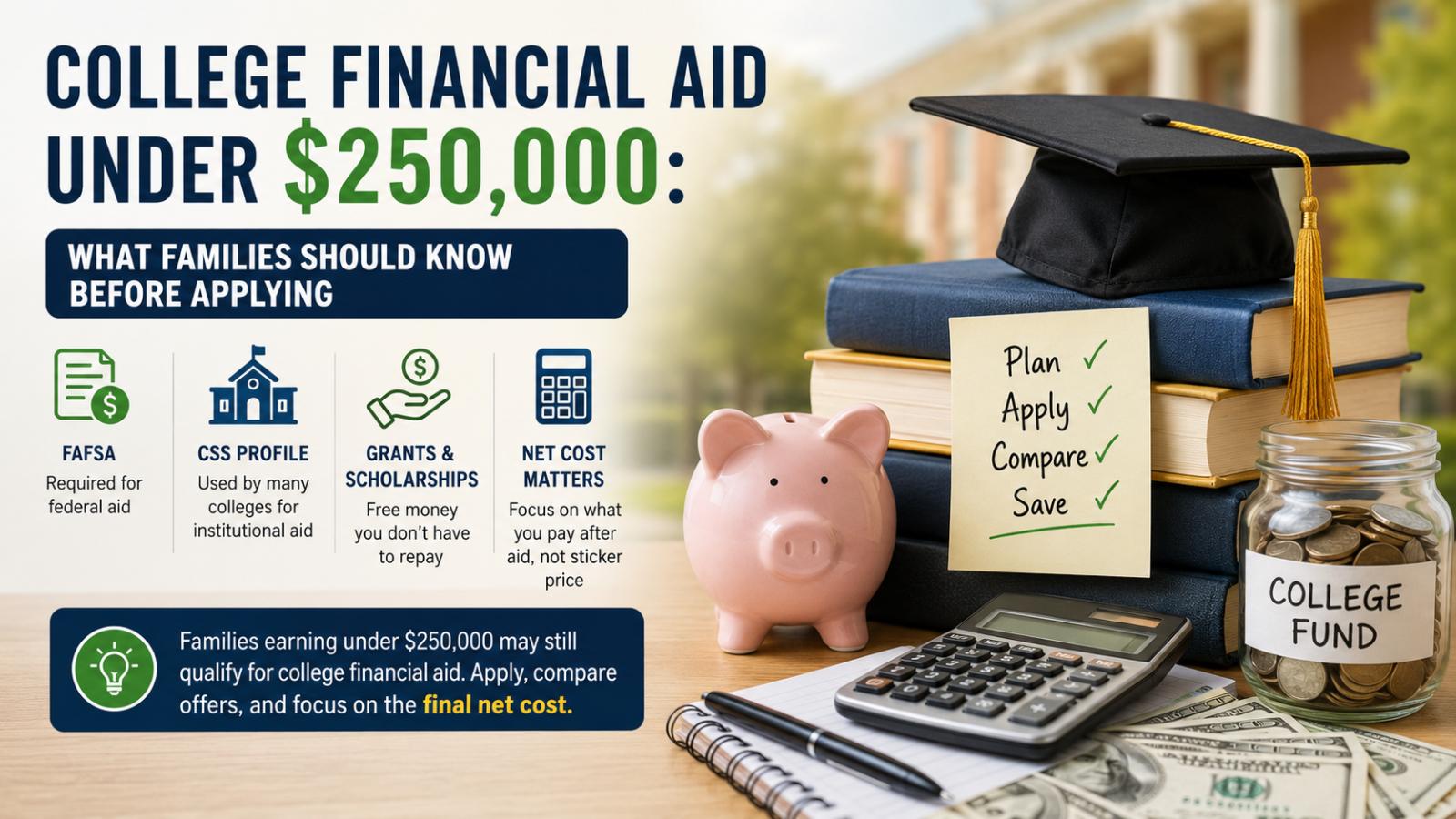

Families earning under $250,000 may still qualify for college financial aid, but the amount depends on the school, household finances, assets, application forms and the college’s total cost of attendance.

There is no single U.S. rule that gives every family below $250,000 free tuition. Some selective private universities offer generous income-based grants, while public colleges and smaller institutions may use different formulas. The final amount often depends on the difference between a family’s calculated ability to pay and the school’s full cost.

Why Families Under $250,000 Should Still Apply

Many middle-income families assume they earn too much to qualify for aid. That can be a costly mistake.

A family earning between $125,000 and $250,000 may not qualify for the same aid as a lower-income household, but tuition, housing, meals, books, fees and travel can still create a major financial burden. At high-cost private colleges, the published yearly price can be far above what a family actually pays after grants and scholarships.

The issue gained attention after the University of Chicago announced on Wednesday, May 13, 2026, that starting in Autumn Quarter 2027 it will guarantee free tuition for undergraduate students from families earning less than $250,000 with typical assets. The university also said families earning less than $125,000 with typical assets may receive support covering tuition, fees, housing and meals.

For more details on the university’s expanded aid policy, read our full report on University of Chicago free tuition for families earning under $250,000

How College Financial Aid Is Reviewed

Most U.S. colleges use the FAFSA, or Free Application for Federal Student Aid, to determine eligibility for federal student aid. Some colleges also use FAFSA information to award state or institutional aid.

The FAFSA now uses the Student Aid Index, or SAI, instead of the older Expected Family Contribution system. The SAI is not the exact amount a family must pay. It is an eligibility index colleges use to help determine financial need. For dependent students, the calculation can include parent income, parent assets, student income and student assets.

Some private colleges also require the CSS Profile. The College Board says the CSS Profile is used by colleges and scholarship programs to award non-federal institutional aid. Schools may have different CSS Profile deadlines, so families must check each college separately.

| Factor | Why It Matters |

|---|---|

| Family income | Helps estimate financial strength |

| Parent assets | Savings and investments may affect aid |

| Student assets | Student-owned savings can also matter |

| Family size | Larger households may show greater need |

| Children in college | May influence institutional aid at some schools |

| FAFSA | Required for federal aid and many college aid offers |

| CSS Profile | Used by many private colleges for institutional aid |

| Cost of attendance | Higher-cost schools may offer larger grants |

| Net price calculator | Helps estimate the real cost after grants |

Why Net Cost Matters More Than Tuition

Families should not judge affordability only by the published tuition price. The better number is the net cost, which is the amount a student pays after scholarships and grants are subtracted.

The U.S. Department of Education defines net price as the amount a student pays for one academic year after subtracting scholarships and grants, which do not need to be repaid. Net price calculators allow families to estimate what similar students paid after grant and scholarship aid.

This is why a college with a $90,000 published cost may sometimes be cheaper than a college with a $45,000 published cost if the higher-priced school offers stronger need-based grants.

A Simple Example for Middle-Income Families

A family earning $180,000 may assume they will receive no help. But if a private university’s total cost is $90,000 a year and the school has a strong need-based aid program, that family may still receive institutional grant aid.

Another family earning the same amount may receive little or no aid at a lower-cost public university, especially if the school has fewer institutional funds. That does not mean the FAFSA was wrong. It means each college has its own cost, aid budget and formula.

This is why families should compare the final aid offer from each college, not just the sticker price.

What Aid Can Cover

College financial aid may include grants, scholarships, work-study, federal loans, state aid or direct institutional support.

Grants and scholarships are usually the most valuable forms of aid because they do not need to be repaid. Loans can help cover costs, but families should review repayment obligations carefully before accepting them.

Some colleges may cover only tuition. Others may also cover required fees, housing and meals for families below certain income limits. Families should read each aid offer closely to understand what is covered and what remains out of pocket.

What Families Should Check Before Applying

Families earning under $250,000 should check whether each college requires FAFSA, CSS Profile or both. They should also review priority deadlines, asset rules, outside scholarship policies and whether aid is renewable each year.

They should also use each college’s net price calculator before deciding whether a school is too expensive. Federal rules require many Title IV institutions enrolling full-time, first-time undergraduate students to provide a net price calculator on their website.

The most important question is not “What is the tuition?” It is “What will this college cost after grants, scholarships and aid?”

Families under $250,000 should not assume they earn too much for college financial aid. The smarter step is to apply, compare offers and focus on the final net cost before making a decision.